Best cyber insurance SaaS startup 2026 options have never been harder to compare — the market has stratified into tech-forward insurtechs that scan your infrastructure before issuing a quote and traditional carriers that compete on capacity and claims-paying strength. This guide breaks down six leading providers — Coalition, At-Bay, Resilience, Cowbell, Corvus (now a Travelers company), and Travelers CyberRisk — on underwriting requirements, coverage structure, premium benchmarks by revenue band, and what distinguishes each when a claim actually hits.

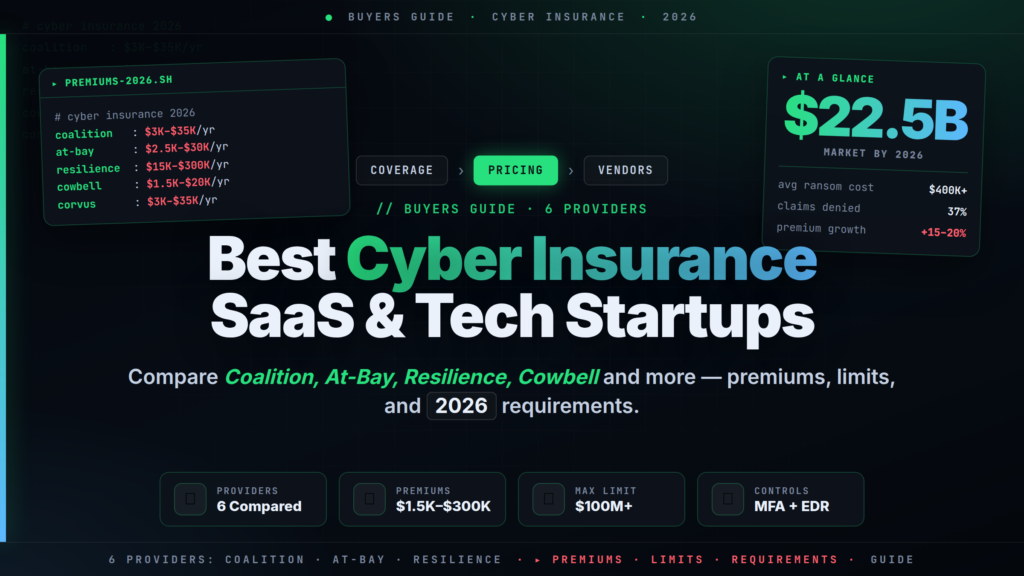

The stakes are not abstract. The global cyber insurance market is projected to reach $22.5 billion by 2026, and average ransomware event costs — ransom payment plus recovery plus business interruption plus legal exposure — routinely reach $1M–$5M for mid-sized businesses, with average US data breach costs across all cost categories exceeding $10M. For SaaS and tech companies processing customer data and dependent on third-party cloud infrastructure, the financial exposure is structural.

// 01 What Cyber Insurance Actually Covers: First-Party vs Third-Party Liability

Cyber insurance has two distinct coverage pillars. Understanding both is essential before comparing providers.

First-party coverage pays for your own losses:

- Ransomware and extortion payments — the ransom itself, plus negotiation support and the cost of the specialist negotiators carriers deploy

- System restoration and data recovery — forensics, re-imaging, and data reconstruction costs

- Business Interruption (BI) — lost revenue during downtime; the trigger is usually a "security event" or "system failure" as defined in the policy

- Dependent Business Interruption — BI caused by a third-party provider outage (AWS, Azure, GCP, Salesforce); this is critical for SaaS companies and is frequently under-insured because it only applies if explicitly endorsed

- Crisis management — public relations costs, breach notification letters, and credit monitoring for affected customers

- Cyber crime / funds transfer fraud — losses from social engineering attacks and BEC (Business Email Compromise, where attackers impersonate executives or vendors to redirect wire transfers)

- Hardware replacement — physical devices destroyed by a destructive attack or wiper malware

Third-party liability coverage pays claims from others:

- Data breach liability — class actions and individual claims following a breach of customer PII (Personally Identifiable Information)

- Regulatory defense and fines — GDPR (General Data Protection Regulation), CCPA (California Consumer Privacy Act), and state breach notification defense costs; note that GDPR fines are excluded or sub-limited in many US-issued policies

- Network security liability — if your compromised infrastructure propagates malware to a customer or partner network

- Tech E&O (Errors and Omissions) — professional liability for software bugs or service failures that cause customer losses; typically sold as a combined Cyber + Tech E&O product, which is directly relevant for SaaS companies

- PCI-DSS fines — card network penalties when a breach exposes cardholder data

Sub-limits are where policies diverge most significantly. Ransomware, social engineering, and dependent BI are routinely capped at 50% of the overall policy limit — or at a specific dollar amount — unless specifically negotiated. On a $5M policy, that can mean only $2.5M is available for what is statistically the most common large-loss claim type.

// 02 Security Controls Underwriters Require in 2026

The underwriting application in 2026 functions as a technical security audit. Carriers run automated external scans of your domains and IP ranges and cross-reference them against the controls you disclose. Misrepresentation is a genuine policy-voiding risk — a May 2026 ruling in Travelers v. ICS confirmed that policies can be voided when insureds materially misrepresent their security posture on the application, an important precedent the whole market is watching.

| Control | Requirement Level in 2026 |

|---|---|

| MFA on email and cloud accounts | Hard requirement; SMS-based OTP increasingly insufficient; app-based or FIDO2 hardware keys preferred |

| MFA on remote access (VPN, RDP) | Hard requirement; RDP exposed directly to the internet is near-automatic decline |

| MFA on all privileged and admin accounts | Hard requirement across all carriers |

| EDR on all endpoints and servers | Hard requirement; legacy antivirus-only protection is no longer accepted |

| 24/7 SOC or MDR monitoring | Required by top-tier carriers for mid-market; strongly preferred for SMBs |

| Immutable or air-gapped offsite backups | Hard requirement; must be documented and tested — evidence of recovery testing required |

| Email authentication (DMARC, DKIM, SPF) | Required; DMARC at reject policy preferred over monitor-only |

| Patch and vulnerability management | Required; evidence of a process is needed, not just attestation |

| Incident Response plan | Required for mid-market; tabletop exercise within prior 12 months preferred |

| PAM (Privileged Access Management) | Required for enterprise accounts; JIT (just-in-time) access documentation is a differentiator |

| Third-party vendor risk management | Required for larger accounts processing third-party data |

Failing these controls does not always result in an outright decline — it results in higher premiums, specific exclusions, or placement in the surplus lines market (non-admitted carriers that operate outside standard rate and form regulations), where premiums can run 2–3× the standard market rate. Companies that let controls slip after binding can also face mid-term premium adjustments from carriers using continuous monitoring, as described in the Cowbell section below.

// 03 best cyber insurance SaaS Startup 2026: The 6 Providers Compared

Coalition

Coalition is the largest of the cyber insurtech MGAs (Managing General Agents — specialty insurers that underwrite on a carrier's paper but manage their own book independently) by written premium in the US. Its defining product is Active Insurance, which bundles a cyber policy with continuous access to Coalition Control — a platform that scans your external attack surface, monitors for exposed CVEs (Common Vulnerabilities and Exposures — publicly disclosed security flaws), and alerts you when leaked credentials appear on dark web markets.

The critical distinction from traditional carriers: Coalition can detect a misconfigured server or a leaked admin password before an attacker does, and notify you before a claim is filed. No traditional insurer offers this at the point of sale.

Coverage limits: Up to $15M per occurrence for mid-market accounts; larger limits available through facultative placement (one-off reinsurance arrangements for accounts exceeding standard capacity).

Premium benchmarks (2026 indicative ranges):

- Under $5M ARR: $3,000–$8,000/year for a $1M limit

- $5M–$50M ARR: $8,000–$35,000/year for $3M–$5M limits

- $50M+ ARR: $35,000–$150,000+/year depending on security posture and data sensitivity

Standout features: Breach coach and 24/7 incident response hotline included; ransomware negotiation support; social engineering / funds transfer fraud available as an endorsement; full-limit ransomware negotiable for strong-controls accounts.

Best for: Series A/B SaaS companies that want a technology monitoring platform paired with coverage and need competitive pricing with integrated breach-response services.

At-Bay

At-Bay operates similarly to Coalition but differentiates on advisory depth — it bundles security awareness training, exposure management, fraud defense tools, and incident response coordination into the policyholder relationship. Monitoring is continuous post-bind, not just at application, via the At-Bay Stance platform.

At-Bay is particularly relevant for SaaS companies because it offers Tech E&O (Errors and Omissions — professional liability coverage for software bugs or service outages that cause customer losses) combined with cyber as a single policy. This removes the need for a separate professional liability placement, simplifying the insurance program and eliminating coverage gaps between two separate policies.

Coverage limits: Up to $10M for SMB and mid-market; up to $25M+ for larger risks.

Premium benchmarks:

- Under $5M ARR: $2,500–$7,500/year for a $1M limit

- $5M–$50M ARR: $7,000–$30,000/year for $2M–$5M limits

- $50M+ ARR: $30,000–$120,000+/year

Standout features: Continuous monitoring post-bind; combined Cyber + Tech E&O option; incident response coordination; network business interruption with dependent BI extensions.

Best for: SaaS companies that need combined Cyber + Tech E&O coverage, and founders who want active security advisory bundled into the premium rather than purchasing it as a separate managed service.

Resilience

Resilience targets middle-market and large enterprises rather than SMBs, and it differentiates on CRQ — cyber risk quantification, a methodology that converts cyber exposure into financial terms expressed as expected annual loss in dollars. Policyholders receive a quantified financial exposure model alongside their policy, which makes Resilience a preferred choice for PE-backed (private equity-backed) portfolio companies and Series C+ firms where boards and audit committees require financial reporting on cyber risk in the same format as other operational risks.

Resilience also operates a Risk Operations Center (ROC) that delivers proactive threat intelligence relevant to the insured's specific technology stack — not reactive incident response after a breach has occurred, but early-warning signals tied to the tools and vendors the company actually uses.

Coverage limits: $5M to $100M+ for their target market segment.

Premium benchmarks:

- Under $5M ARR: Generally minimum premiums price Resilience out of this band — it is better suited to mid-market and above

- $5M–$50M ARR: $15,000–$60,000/year for $5M–$10M limits

- $50M+ ARR: $50,000–$300,000+/year for $10M–$50M limits

Standout features: CRQ reporting for board and investor audiences; Risk Operations Center with proactive threat intel; claims advocacy team; business interruption with dependent BI; incident response plan review and tabletop exercise support.

Best for: Series C+ companies, PE-backed tech firms, and enterprise accounts that need deep underwriting, large limits, and quantified risk reporting for governance audiences.

Cowbell

Cowbell targets SMBs with an AI-driven continuous underwriting model built on Cowbell Factors — a proprietary risk score that updates in real time based on automated scanning of the insured's external attack surface and disclosed security controls. Cowbell is the most accessible carrier in this comparison for companies that have not yet deployed a full security stack: its underwriting requirements are calibrated to SMB realities rather than demanding enterprise-grade MDR (Managed Detection and Response) 24/7 coverage as a prerequisite.

One important feature to understand: Cowbell's adaptive pricing model allows the carrier to adjust premiums mid-term if your Cowbell Factors score degrades significantly — a mechanism that can work against you if security controls slip after binding.

Coverage limits: Up to $6M for SMBs; mid-market limits available for larger accounts.

Premium benchmarks:

- Under $5M ARR: $1,500–$5,000/year for $500K–$1M limits — the lowest entry price in this comparison

- $5M–$50M ARR: $5,000–$20,000/year for $1M–$3M limits

- $50M+ ARR: $20,000–$80,000/year

Standout features: CowbellCare pre-breach services including security awareness training and dark web monitoring; ransomware sub-limit negotiable; adaptive mid-term premium adjustment based on risk score.

Best for: Pre-seed and seed-stage startups with limited security resources that need affordable coverage while building out their controls infrastructure. Also suitable for bootstrapped SaaS companies with moderate revenue but lean security teams.

Corvus (Now a Travelers Company)

Corvus was acquired by Travelers in 2024, making it a technology-forward MGA operating with one of the largest commercial insurance balance sheets in the US behind it. The Corvus brand and platform are preserved. The Corvus Scan platform continuously monitors your external exposure for unpatched CVEs, misconfigured services, open ports, and credential leaks — and delivers those findings to the insured throughout the policy year, not only at renewal.

The Travelers acquisition matters for two practical reasons. First, capacity: higher limits are directly available without external facultative reinsurance arrangements. Second, financial strength: Travelers carries an A++ AM Best rating, which matters for tech startups whose enterprise customer contracts require the insurer to hold a specific financial strength rating — a requirement that some MGA-structured insurtechs cannot satisfy on their own paper.

Coverage limits: Up to $25M+ on primary; larger limits available in tower arrangements (multiple carriers sharing coverage of a single large risk).

Premium benchmarks:

- Under $5M ARR: $3,000–$8,000/year for a $1M limit

- $5M–$50M ARR: $8,000–$35,000/year

- $50M+ ARR: $30,000–$150,000+/year

Standout features: Ongoing CVE scanning and pre-claim threat intelligence feeds; breach coach and incident response panel; business interruption with system failure trigger; Tech E&O combined option available.

Best for: Companies that want a technology-forward underwriting experience but also require Travelers' financial strength rating on the certificate of insurance for enterprise vendor contracts.

Travelers CyberRisk

Travelers CyberRisk is a separate product line from Corvus and targets mid-market through enterprise accounts across all industries through traditional independent broker channels. Unlike the insurtechs above, Travelers CyberRisk involves more manual underwriter review — but this comes with greater flexibility to negotiate specific policy terms, endorsements, and manuscript (custom-drafted) coverage language.

Travelers offers two cyber products: CyberFirst Essentials for small businesses (coverage can be bundled into a BOP — Business Owners Policy — with limits up to $1M–$2M) and CyberRisk for mid-market and enterprise accounts. CyberRisk covers the full suite of first-party and third-party exposures plus post-loss loss control services, and it has one of the most established claims-paying track records in the market.

Coverage limits: $5M–$50M+ on CyberRisk; $1M–$2M on CyberFirst Essentials; enterprise tower programs can reach $100M+.

Premium benchmarks:

- Under $5M ARR: $2,000–$6,000/year for a $1M limit

- $5M–$50M ARR: $8,000–$40,000/year

- $50M+ ARR: $40,000–$200,000+/year

Standout features: Deepest claims-paying history of any carrier in this list; very high limit capacity; post-loss loss control advisory; broker-negotiated manuscript endorsements available.

Best for: Enterprise-level companies requiring very high limits, proven claims-paying history, and the ability to negotiate bespoke policy language through an established broker relationship.

// 04 Premium Benchmarks by Revenue Band

The table below aggregates 2026 indicative premium ranges from Munich Re's cyber insurance market report and carrier-specific data. S&P Global projects 15–20% premium increases in 2026 following two years of rate softening, driven by a 126% increase in ransomware incidents in Q1 2025 and average ransomware event total costs exceeding $1M–$5M for mid-sized companies.

| Provider | Under $5M ARR | $5M–$50M ARR | $50M+ ARR | Max Primary Limit |

|---|---|---|---|---|

| Coalition | $3K–$8K/yr | $8K–$35K/yr | $35K–$150K+/yr | $15M |

| At-Bay | $2.5K–$7.5K/yr | $7K–$30K/yr | $30K–$120K+/yr | $25M |

| Resilience | Not target market | $15K–$60K/yr | $50K–$300K+/yr | $100M+ |

| Cowbell | $1.5K–$5K/yr | $5K–$20K/yr | $20K–$80K/yr | $6M |

| Corvus (Travelers) | $3K–$8K/yr | $8K–$35K/yr | $30K–$150K+/yr | $25M+ |

| Travelers CyberRisk | $2K–$6K/yr | $8K–$40K/yr | $40K–$200K+/yr | $100M+ |

All figures are indicative annual premiums in USD. Actual premiums depend on revenue, industry vertical, data sensitivity, controls maturity, claims history, and carrier appetite at time of submission.

// 05 Key Sub-Limits to Negotiate Before You Sign

The headline policy limit is not the amount available for every loss. Three sub-limits drive the majority of disputes at claims time — and all three are negotiable before you bind.

Ransomware sub-limit: Many policies cap ransomware payments and related recovery costs at 50% of the overall policy limit. On a $5M policy, that is $2.5M available for what is statistically the most common and expensive claim type. Ransomware accounts for approximately 81% of claims involving recovery expense losses. Negotiate to bring the ransomware sub-limit to parity with the overall limit — some insurtechs now offer full-limit ransomware for accounts with strong controls.

Dependent Business Interruption (Dependent BI): SaaS companies have direct financial exposure to third-party cloud provider outages. If AWS goes down for twelve hours and your platform is unavailable to customers, that is a business interruption event — but many policies exclude or severely sub-limit Dependent BI unless specifically endorsed. Ask explicitly: "What is the Dependent BI sub-limit, and does it name AWS, Azure, and GCP as covered providers?"

Social engineering and funds transfer fraud: Standard limits are often $100,000–$500,000 unless specifically endorsed to a higher amount. BEC (Business Email Compromise) attacks targeting tech startups routinely produce six-figure wire transfers to attacker-controlled accounts — losses from BEC attacks globally exceeded $2.9 billion in 2023 FBI IC3 data, with the figure rising annually. For any company processing vendor payments, payroll, or customer refunds, negotiate this sub-limit to at least $1M.

// 06 Provider Selection: Matching Carrier to Stage

The diagram below maps company stage to the most likely best-fit providers based on revenue band and security maturity.

Pre-seed and seed stage (under $5M ARR): Cowbell is the most accessible entry point — its AI-driven underwriting accommodates companies that have not yet deployed full EDR or 24/7 SOC coverage, and its entry pricing is the lowest in this group. At-Bay is the stronger choice if you are already running endpoint protection and want continuous monitoring bundled into the policy relationship.

Series A and B ($5M–$50M ARR): Coalition or At-Bay are the natural fit for tech-forward SaaS companies at this stage. Coalition's Active Insurance platform provides genuine security value beyond indemnity — automated alerts on exposed assets before they are exploited. At-Bay's combined Cyber + Tech E&O option removes the need for a separate professional liability placement, which simplifies the insurance program and eliminates gaps between two policies triggered by the same incident.

Series C+ and PE-backed companies ($25M–$100M ARR): Resilience's cyber risk quantification model produces the board-ready financial impact reports that governance audiences require. The Risk Operations Center delivers the kind of proactive threat intelligence that security-mature companies expect from a strategic partner, not just a claims payer.

Enterprise and high-limit requirements ($100M+ ARR or vendor contracts requiring a specific carrier rating): Travelers CyberRisk or Corvus — now operating with Travelers' A++ AM Best balance sheet — are the strongest options. Many enterprise B2B customer contracts require the insurer to hold a minimum financial strength rating; some insurtechs operating as MGAs on third-party paper cannot satisfy this requirement.

// 07 The Claims Reality: What the Numbers Say

Before selecting a provider, understand the base rates for the market. 37% of cyber insurance claims are denied or partially excluded — the leading cause is a gap between controls the insured attested to on the application and controls actually deployed at time of loss. The Travelers v. ICS ruling makes clear that this gap is not just a coverage dispute; it is grounds for policy avoidance.

A second data point worth noting: 27% of data breach claims involved exclusions that resulted in non-payment or partial payment. The most common exclusion triggers are war/nation-state exclusions (contested in incidents involving Russian or Chinese threat actors), contractual liability exclusions (losses arising from SLAs or indemnification clauses in customer contracts), and the infrastructure failure exclusion (losses from cloud provider outages that are not specifically endorsed as Dependent BI events).

The actionable implication: when you compare providers, read the exclusions as carefully as you read the insuring agreement.

// 08 Conclusion

The best cyber insurance SaaS startup 2026 decision ultimately depends on three variables: your revenue band, your current security controls maturity, and how much platform value — continuous monitoring, threat intelligence, advisory services — you want embedded in the premium you pay.

For early-stage companies, Cowbell or At-Bay offer the lowest friction to get covered with reasonable limits. For Series A/B, Coalition or At-Bay deliver genuine security ROI alongside indemnity. For larger companies and PE-backed portfolios, Resilience or Travelers bring the capacity, reporting depth, and financial strength the risk requires.

Before binding any policy: negotiate ransomware sub-limits to parity with the overall limit, confirm your dependent BI endorsement covers your cloud providers by name, and ensure social engineering limits are sized for your actual payment volumes. Verify that every control you attest to on the application is documented and deployed — the 37% claim denial rate in this market is not a coincidence.

See our analysis of the attack types your cyber policy is designed to cover: how Cordial Spider executes vishing and SSO hijacking against SaaS targets, and why ransomware groups are getting more aggressive against infrastructure targets. For a deeper look at the security controls underwriters are testing at renewal, see Zero Trust and data movement gaps.

Subscribe to our weekly threat digest to stay current on claims trends and underwriting shifts that affect your next renewal →

For any query contact us at contact@cipherssecurity.com